Tax Enquiries

HMRC General Enquiries

HMRC has extensive investigative powers to enquire into and challenge the tax liability of individuals and companies, including conducting both civil and criminal tax investigations. If you or your client are deemed by HMRC to have paid an insufficient amount of tax, then HMRC may also be able to impose penalties for careless and deliberate errors.

HMRC Investigations

What Triggers a Tax Enquiry

Enquiries are usually opened for one of two reasons:

Tax enquiry for cause, namely:

- There is something wrong on the face of the return that gives HMRC some cause for concern;

- HMRC has information from other sources that conflicts with what is shown on the return (e.g., information disclosed under a tax treaty, tip-off, ex-partner, trading platform);

Tax enquiry on a random basis:

- The taxpayer’s return is randomly selected for enquiry by an HMRC computer.

What are HMRC’s Sources of Information Regarding Tax?

HMRC has access to a considerable volume of information which enables them to identify potential errors in a tax return and/or the failure to pay the correct amount of tax. These sources of information include:

- “Connect”, which is an IT program that sifts information, coverings details of bank interest, credit card data, DVLA and Land Registry reports relating to individuals and companies

- HMRC data gathering powers under Finance Act 2011, Sch. 23

- HMRC has acquired the right to force apps and platforms such as Apple, Amazon and Airbnb to hand over data — including names and addresses of sellers and advertisers

- Payment providers such as PayPal are another source of data

- International co-operation: information provided by non-UK tax authorities under tax treaties or other exchange of information agreements(e.g. see IEIM300000 – International Exchange of Information Manual – HMRC internal manual – GOV.UK (www.gov.uk))

- Informants

- Information Leaks

- “Panama” papers

- “Paradise” papers

- Suspicious activity reports (SARs) under the anti-money laundering legislation

- If a bank or professional adviser has any suspicion that a customer might be involved in money laundering or terrorist financing, they are obliged to alert law enforcement agencies

- Common Reporting Standard (the “CRS”) which came into effect in 2018 and provides HMRC with more information on offshore accounts

HMRC Tax Enquiry Time Limits

If HMRC decides to open a tax enquiry against your client or you as an adviser, they must do so in accordance with the statutory provisions for the particular tax under investigation. The time limit is generally 12 months, though can be up to two years for VAT. Generally, if HMRC has run out of time to open an enquiry, then they can only issue an assessment if they have made a discovery.

Income and Capital Gains Tax returns

- Individuals and Sole Traders: Section 9A TMA 1970 requires that an enquiry is opened within 12 months of the return being delivered to HMRC

- Partnerships: Section 12AC TMA 1970: requires that an enquiry is opened within 12 months of the return being delivered to HMRC

Corporation Tax returns

- Companies – Paragraph 24(1) Schedule 18 FA 1998 requires that an enquiry is opened within 12 months of the Company Tax Return being delivered to HMRC

SDLT

- FA 2003, Sch. 10, para. 12: HMRC must open an enquiry within 9 months of the filing date of the return

VAT

- Assessment must be made not later than 2 years after the end of the prescribed accounting period or 1 year “after evidence of facts, sufficient in the opinion of the Commissioners to justify the making of the assessment comes to their knowledge.”

Can a Tax Enquiry be brought to an End?

This depends on the nature of the tax involved. Some statutory provisions, such as those relating to income tax, capital gains tax, corporation tax and stamp duty land tax enable a taxpayer to apply to the First-tier Tribunal for a direction that the enquiry is brought to an end within a specified period.

In relation to such taxes, there is a presumption in favour of the taxpayer’s application that:-

“The tribunal shall give a direction unless satisfied that an officer of Revenue and Customs has reasonable grounds for not giving a closure notice within a specified period.”

The First-tier Tribunal guidance on closure notice applications is available here:

If you feel an HMRC investigation has dragged on longer than is reasonably necessary, you can make an application to close the enquiry. Your reasons for wanting closure could include:

- The enquiry has become very long without justification

- The enquiry has become expensive, in respect of:

- The taxpayer/management time

- Third-party adviser costs:

- Accountants

- Legal advisers

- Commercially disruptive

- The risk that if an appeal is not progressed then evidence will become stale and less valuable in proving the taxpayer’s case

- The risk that other weak cases on the facts will be decided first, resulting in legal principles which are unhelpful to the taxpayer’s appeal

- Risk that on selling a business the purchaser retains a percentage of the consideration or reduces the purchase price due to perceived unresolved tax liabilities (which may at a hearing subsequently not be crystallised)

Before making an application to bring an enquiry to an end, you should ask yourself the following questions. These are relevant to deciding whether HMRC has reasonable grounds for not giving a closure notice.:

- What information has been provided to HMRC, and when?

- Has the taxpayer been co-operative?

- Has the enquiry proceeded to a point where HMRC can make an informed decision as to the matter in issue?

- Would it be proportionate to issue a closure notice given the length of time that has passed since the opening of the enquiry?

- What is the burden placed on the taxpayer by the length of the enquiry/is it disproportionate?

- Is the taxpayer asking for a closure notice by reference to a “specified period” that is reasonable to allow resolution on any material outstanding issues? (asking for an enquiry to be closed immediately is rarely reasonable, but asking for closure within 2 to 3 months is likely to be appropriate, subject to the circumstances of the case)

- Can the taxpayer demonstrate that HMRC’s legitimate concerns have been addressed/information provided on a timely basis?

Tax Assessment Time Limits

Under the present discovery regime, the basic rules for income tax, capital gains tax and corporation tax are that tax assessments cannot be validly issued after:

- 4 years, unless one of the following applies;

- 6 years for a careless error

- 20 years for a deliberate error

These time limits apply from the end of the accounting period or tax year. The time limits for taxpayer claims are also aligned at four years.

What does an HMRC Tax Enquiry Cover?

HMRC will usually send a letter to the taxpayer and their authorised agent giving notification that a return is to be checked. At this stage, there are several key points you should consider:

- Check that HMRC is within the statutory time limits for opening an enquiry or that there is a discovery as a matter of law.

- Is the information requested something which HMRC are entitled to as part of the taxpayer’s tax records, and is the information request reasonable under FA 2008, Sch.36?

- Check you/your adviser can comply with any timescale for providing information.

- Carry out a review of the tax position to ensure that the position is accurate, and if not, identify the reason for any defect in the return.

- Obtain specialist professional legal and/or accounting advice as soon as possible.

- Identify the types of tax technical challenge and how they can be answered.

- Draw up a list of the information you require, including possible information from third parties.

- Consider making a payment on account of tax to limit interest and penalties (to the extent any tax insufficiency is identified, but not capable of precise quantification).

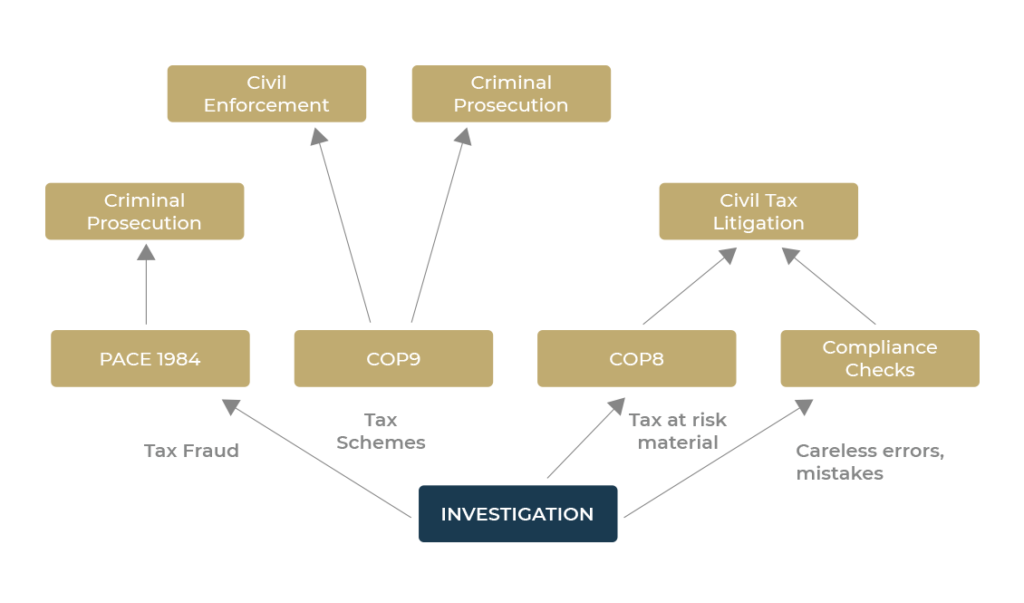

Code of Practice 8 Enquiries / COP8

A COP8 enquiry is dealt with by HMRC’s Fraud and Avoidance department within the Special Investigations Office. COP8 applies where the ‘tax at risk’ involves a potential minimum of £500,000 extra tax, interest and penalties, and/or there are complex technical matters/tax avoidance arrangements.

HMRC’s guidance on COP8 investigations is available here: Specialist investigations for fraud and bespoke avoidance: Code of Practice 8 – GOV.UK (www.gov.uk)

Code of Practice 9 Enquiry / Cop9 / Tax Fraud

A COP9 is HMRC’s enquiry into suspected cases of tax fraud. Tax fraud is an intentional act by a person not to report the correct amount of tax for personal gain at the expense of the public. Under a COP9 investigation, the taxpayer is offered an opportunity to make full and complete disclosure of all tax irregularities. In exchange, HMRC will not seek a criminal prosecution for any tax fraud committed in any period before the date when they first informed the person under investigation of their decision to investigate using COP9 procedures. Under a COP9 the taxpayer has 60 days to provide full and frank disclosure of the tax fraud.

HMRC’s guidance on COP 9 investigations is available here:

Code of Practice 9: where HM Revenue and Customs suspect fraud (COP9) – GOV.UK (www.gov.uk)

Are Tax Investigations made Public?

Tax investigations do not usually result in a taxpayer’s affairs being made public. If a taxpayer appeals against a closure notice or assessment, then the proceedings in the First-tier Tribunal will be in the public domain (including any First-tier Tribunal decision (these can be accessed here: Tax tribunal decisions – GOV.UK (www.gov.uk)). A criminal prosecution arising from a criminal investigation will also be in the public domain.

HMRC has a ‘Name and Shame’ policy for deliberate tax defaulters which is authorised under the Finance Act 2009, section 94. This means HMRC may publish information about any person if:

in consequence of an investigation conducted by the Commissioners, one or more relevant tax penalties is found to have been incurred by the person, and

the potential lost revenue in relation to the penalty (or the aggregate of the potential lost revenue in relation to each of the penalties) exceeds £25,000.

A “relevant tax penalty” is:

- a penalty under paragraph 1 of Schedule 24 to FA 2007 (inaccuracy in taxpayer’s document) in respect of a deliberate inaccuracy on the part of the person,

- a penalty under paragraph 1A of Schedule 24 to FA 2007 (inaccuracy in taxpayer’s document attributable to the deliberate supply of false information or deliberate withholding of information by person),

- a penalty under paragraph 1 of Schedule 41 to FA 2008 (failure to notify) in respect of a deliberate failure on the part of the person, or

- a penalty under paragraph 2 (unauthorised VAT invoice), 3 (putting product to use attracting higher duty etc) or 4 (handling goods subject to unpaid excise duty) of Schedule 41 to FA 2008 in respect of deliberate action by the person.

The current list of deliberate tax defaulters can be accessed at this link:

Details of deliberate tax defaulters – GOV.UK (www.gov.uk)